How Independent Directors and Engineers Bridge the Gap Between Compliance and Corruption

This paper examines the structural decay of oversight institutions and proposes systemic reforms to restore genuine independence in corporate boards and public projects.

Executive Summary

The rise of “independent” oversight—through directors in corporate boards and engineers in public projects—was meant to safeguard integrity, transparency, and public trust. Yet in practice, these guardians have become toothless tigers, symbolizing the illusion of independence in India’s governance ecosystem. Both roles were conceived as buffers against conflict of interest, but have been structurally weakened by dependence on the very entities they are meant to oversee.

In corporate India, independent directors often serve at the pleasure of promoters; in public works, independent engineers rely on project authorities for contracts and payments. The result is a silent compliance economy—where watchdogs bark only when convenient, and systemic corruption thrives beneath layers of procedural legitimacy.

This article examines how “independence” has been monetized, turning oversight into a transactional bridge between compliance and corruption. It calls for a rethink of accountability frameworks—where independence is not just a designation, but a design of power, protection, and public purpose.

1. Introduction

“Independence” is the aspirational linchpin of modern governance. Independent directors in corporate boards and independent engineers in public infrastructure are conceived as the institutional firewall between public purpose and private rent‑seeking. In theory, they dilute conflicts of interest, strengthen fiduciary care, and keep projects aligned with specifications, budgets, and timelines.

In practice, however, many of these guardians function as ceremonial placeholders. Their powers are weak, their resourcing thin, and their tenure contingent on the goodwill of those they are meant to scrutinize. This gap between design and delivery converts “independence” into a legitimacy‑laundering device: the mere presence of an independent actor becomes a certificate of integrity, even when substantive accountability is absent.

This paper asks a simple question with complicated implications: why do supposedly independent directors and engineers so often become toothless tigers? It synthesizes statutory expectations, incentive structures, field dynamics, and emblematic case studies to show how oversight is routinely neutralized. It concludes with a reform agenda that treats independence as a design of power—appointments, tenure, pay, data access, reporting rights, and liability—rather than a nominal title.

1A. Historical Evolution of Oversight

The ideal of institutional independence traces its lineage to both Western corporate reform and Indian administrative philosophy. In Britain, the Cadbury Report (1992) formalized non‑executive directors as custodians of shareholder interest after governance scandals. In the United States, the Sarbanes–Oxley Act (2002) mandated independent audit committees and stricter disclosure following Enron and WorldCom.

In India, independence entered corporate governance through SEBI’s Clause 49 and later the Companies Act (2013). Public projects adopted the Independent Engineer model from FIDIC,World Bank and ADB frameworks to arbitrate between contractor and client. Over time, however, political patronage and contractual dependence transformed these guardians from neutral referees into instruments of procedural legitimacy.

2. The Promise and Prescription of Independence

Independence rests on the assumption that distance breeds objectivity. In corporate governance, independent directors act as fiduciary stewards, chairing audit and risk committees under the Companies Act (2013) and SEBI’s LODR Regulations. In public projects, Independent Engineers (IEs) review designs, inspect works, certify milestones, and adjudicate disputes—imported from multilateral procurement frameworks to balance cost, quality, and time.

The intended promise: checks and balances, credible governance, continuity across leadership cycles, and a blend of technical and ethical correctives. The prescriptive frameworks look robust on paper, but practice has inverted them; independence often functions as presence without power.

3. The Political Economy of Oversight

Behind failed oversight lies a political economy that rewards silence. The principal–agent problem persists when the monitor is paid by the monitored. Rent‑seeking equilibria distribute gains safely under legitimacy cover. Moral hazard and network capture make dissent costly and compliance rewarding, while information asymmetry blinds external monitors who lack data rights and field time.

How Independence Gets Captured

Appointment Dependence

↓

Information Asymmetry

↓

Soft Coercion (Payments, Tenure)

↓

Ritual Compliance

↓

Legitimacy Shield (Use of Independence as Cover)

↓

Crisis / Scapegoating / Exit

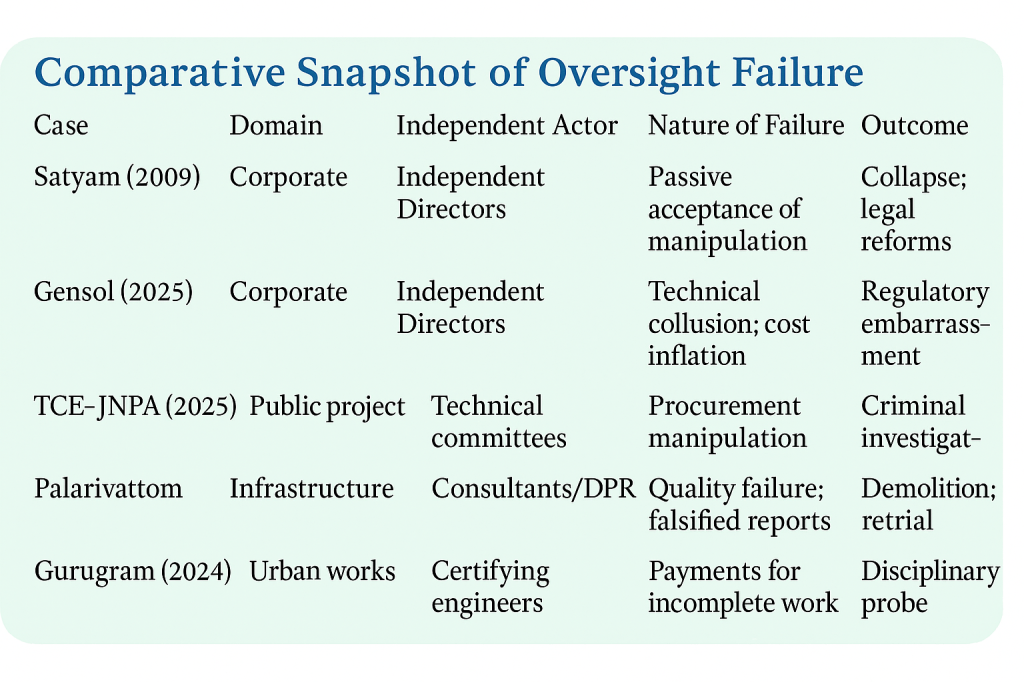

4. Case Studies: When “Independence” Failed

Corporate case studies reveal that independence on paper often dissolves in practice. In boardrooms across India, independent directors—intended as sentinels of governance—are frequently reduced to spectators. The Satyam scandal showed how prestige replaced prudence; Gensol’s resignations exposed the fragility of accountability when promoters hold the purse strings. Across industries, independent directors face a structural dilemma: they are expected to challenge those who appoint and compensate them. As a result, their oversight frequently ends where confrontation begins.

A similar pattern echoes across public infrastructure, where Independent Engineers (IEs), designed to serve as neutral arbiters between contractor and client, face parallel pressures. Their contracts are financed and renewed by the very authorities they monitor, transforming independence into dependence by design. From expressways and smart city projects to ports and bridges, the IE system mirrors the same conflict-ridden architecture that weakens corporate boards. The erosion of independence—through data opacity, financial subordination, and procedural capture—has made both directors and engineers complicit participants in the theatre of compliance rather than agents of accountability.

4.1 Satyam (2009): Board‑Level Oversight Breakdown

Founder Ramalinga Raju’s confession exposed inflated assets and fictitious cash balances. Multiple independent directors approved related‑party transactions, reflecting over‑reliance on management disclosures and audit assurances (Reuters 2009; TaxGuru 2023).

4.2 Gensol Engineering (2025): Resignations Under Regulatory Heat

After SEBI barred the promoters for alleged fund misuse, three independent directors resigned, signalling the fragility of independence when underlying power lies elsewhere (Reuters 2025).

4.3 Tata Consulting Engineers & JNPA Dredging (2025): Alleged Estimate Inflation

A CBI FIR alleged collusion between the PMC and officials to inflate estimates and curb competition, pegging losses at roughly ₹800 crore. Independent technical opinions were reportedly sidelined (India Today 2025).

4.4 Megha Engineering & NMDC/MECON/NISP (2024): Procurement Integrity Probe

CBI alleged bribery and undue influence in a ₹315‑crore contract, illustrating how technical adjudication and certification can be polluted, rendering independent oversight ineffective (Indian PSU 2024).

4.5 Palarivattom Flyover (Kerala): Early Failure and Partial Demolition

Structural defects soon after inauguration raised questions about consultant independence, DPR quality, and oversight; technical risk signals were reportedly ignored or muted (Wikipedia 2020; The Hindu 2020).

4.6 Municipal Engineering Failures (Gurugram): Everyday Capture

Vigilance probes found payments cleared for incomplete or substandard works, echoing a pattern where certifying engineers functioned as rubber stamps rather than guardians (Times of India 2024).

4.7 Delhi–Meerut Expressway (2019): Disputed Certification and Delays

The IE appointed for the ₹7,500-crore Delhi–Meerut Expressway faced allegations of certifying incomplete work packages and approving milestone payments before field verification. A later CAG audit (2021) found cost escalation and delayed rectification, revealing the IE’s limited leverage against politically driven timelines. The case showed that contractual dependence on NHAI compromised independent assessment.

4.8 Smart City Mission (2020–2023): Cosmetic Compliance in IE Reports

Several Smart City projects (e.g., Bhopal, Pune, Lucknow) appointed Independent Engineers for third-party quality control. However, RTI responses and local audits showed identical wording in multiple city reports—suggesting “template oversight.” Engineers faced informal pressure to fast-track certifications so that progress dashboards met central reporting targets. The IE function effectively became a compliance rubber stamp rather than a quality safeguard.

4.9 Mumbai Coastal Road Project (2022): Oversight Overruled

The IE consortium flagged potential marine ecological risks and foundation deviations during piling. Instead of enforcing corrections, the contractor and project authority reportedly sidelined the warnings, citing “urgency.” The IE’s dissent notes were not published, illustrating how contractual independence without statutory backing leaves oversight voiceless in megaprojects.

4.10 Bihar Bridge Collapse (Aguwani –Sultanganj, 2023): Invisible Oversight Chain

After the under-construction bridge collapsed twice in two years, investigations found that the IE had repeatedly flagged design inconsistencies and material deviations, but the correspondence never reached the project authority’s top desk. The IE’s contract had no escalation clause. The episode epitomized the IE’s role as an unheeded messenger in politically sensitive projects.

4.11 Navi Mumbai Airport (Ongoing): Performance Oversight by Design

Industry observers note that the IE framework for this PPP project is financially tied to milestone clearances. The more milestones certified, the faster the IE gets paid. This structural flaw incentivizes leniency and speed over rigour, making “independence” financially self-defeating.

5. How Independent Roles Bridge Compliance and Corruption

Independence was designed as the bridge between power and accountability, yet captured systems convert it into the bridge between compliance and corruption. Directors sign minutes and RPT approvals; engineers certify milestones—satisfying formal checklists while substantive quality and integrity decay beneath the surface.

The presence of independent signatures deflects blame—“the independent engineer certified it.” When scandals erupt, independents either absorb blame or resign, offering distance without remedy. The result is compliance theatre.

6. Reforming Independent Oversight: From Symbolism to Substance

A functional framework rests on three pillars: Structural Insulation, Transparency Backbone, and Integrity Incentives. Together, these transform independence from ritual to reinforcement.

6.1 Structural Insulation

• Insulated appointments via regulator‑convened panels; prevent promoter/department capture.

• Fixed, non‑renewable tenure to remove re‑appointment pressure.

• Independent remuneration pools (escrow) overseen by regulators or trustees.

• Protected removal requiring disinterested shareholder vote or transparent justification.

6.2 Transparency Backbone

• Public dashboards for inspection reports, IE certifications, and board minutes (redacted).

• Digital twins and IoT sensors for real‑time verification of progress and quality.

• Citizen and professional audits of randomised project samples.

• RTI parity for PPP/SPV entities handling public funds.

6.3 Integrity Incentives

• Safe‑harbour clauses protecting good‑faith dissent and escalation.

• Public recognition and awards for substantive oversight interventions.

• Penalties for habitual rubber‑stamping and wilful blind spots.

• Rotation of independents; meta‑audit to ‘audit the auditors’.

Reform Architecture Model

Structural Insulation

↓

Transparency Backbone

↓

Integrity Incentive Model

↓

→ Trustworthy Governance ←

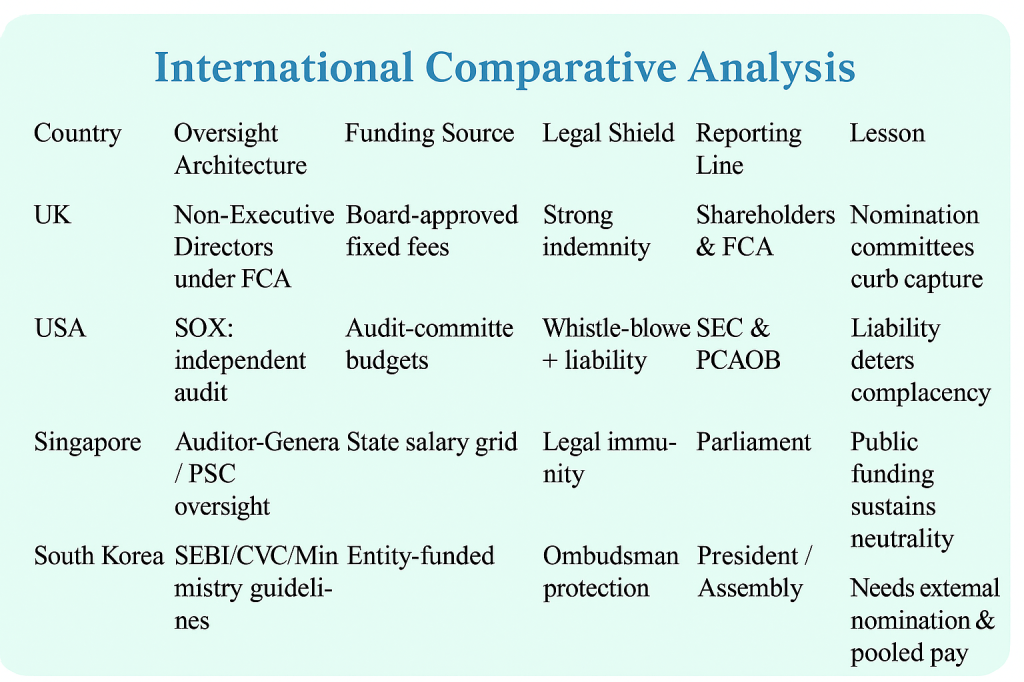

6A. International Comparative Analysis

Comparative practice shows that jurisdictions which truly empower independence design it into law, money, and reporting lines. The following table summarises structural contrasts and lessons for India.

7. Policy Summary and Conclusion

Five Levers for Real Independence:

1) Insulated Appointments

2) Independent Funding

3) Mandated Escalation

4) Transparent Dissent & Disclosure

5) Rotational Oversight & Citizen Access

Each lever closes a fracture in the oversight chain: appointments insulated from capture, money separated from influence, escalation made mandatory, dissent made visible, and roles refreshed to resist capture. Together they convert independence from a personal virtue into a systemic guarantee.

True independence is freedom from consequence in the public interest: the ability to speak truth without reprisals. Without structural redesign, boards and projects will continue to parade toothless tigers while integrity erodes.

References and Sources

Cadbury Committee (1992) Report of the Committee on the Financial Aspects of Corporate Governance. https://ecgi.global/sites/default/files/bromley/files/cadbury_code_1992.pdf

Clarke, T. (2007) International Corporate Governance: A Comparative Approach. Routledge. https://www.routledge.com/International-Corporate-Governance/Clarke/p/book/9780415324833

Government of India (2013) Companies Act 2013. Ministry of Corporate Affairs. https://www.mca.gov.in/content/mca/global/en/acts-rules/companies-act/companies-act-2013.html

Hood, C. (2011) The Blame Game: Spin, Bureaucracy, and Self‑Preservation in Government. Princeton. https://press.princeton.edu/books/paperback/9780691156199/the-blame-game

Power, M. (1997) The Audit Society: Rituals of Verification. OUP. https://global.oup.com/academic/product/the-audit-society-9780198296034

Flyvbjerg, B. (2023) How Big Things Get Done. Currency. https://www.penguinrandomhouse.com/books/704840/how-big-things-get-done-by-bent-flyvbjerg-and-dan-gardner/

Ng, T. & Pierce, L. (2021) The psychological costs of organizational wrongdoing. Annual Review of Psychology. https://www.annualreviews.org/doi/10.1146/annurev-psych-062520-122309

Sethuraman, S. & Kothari, V. (2024) Liability of Independent Directors in India. NUJS Law Review. https://nujslawreview.org/2024/08/10/liability-of-independent-directors/

Azmi, R. & Khosrow‑Panah, I. (2017) Blockchain for public procurement transparency. arXiv. https://arxiv.org/abs/1701.06426

World Bank (2010) Fraud and Corruption Awareness Handbook for Civil Works. https://documents.worldbank.org/en/publication/documents-reports/documentdetail/806391468151785501/fraud-and-corruption-awareness-handbook-for-civil-works

Reuters (2009) Timeline: Satyam’s scandal shakes India Inc. https://www.reuters.com/article/us-satyam-idUSTRE50E2RY20090115

Reuters (2025) Independent directors exit Gensol after co‑founders probed, 18 April. https://www.reuters.com/world/india/independent-directors-exit-indias-gensol-after-co-founders-probed-2025-04-18/

India Today (2025) CBI case against Tata Consulting Engineers and officials in ₹800‑crore project fraud. https://www.indiatoday.in/india/story/cbi-case-against-tata-consulting-engineers-government-officials-in-rs-800-crore-project-fraud-2743829-2025-06-20

Indian PSU (2024) CBI FIR against Megha Engineering and officials of NMDC, MECON, NISP. https://indianpsu.com/cbi-fir-against-megha-engineering-and-ten-officials-of-nmdc-mecon-and-nisp-for-corruption-in-rs-315-crore-project/

Times of India (2024) Payments cleared for incomplete works: 12 MCG engineers under scanner. https://timesofindia.indiatimes.com/city/gurgaon/payments-done-work-incomplete-12-mcg-engineers-under-scanner/articleshow/120909748.cms

Wikipedia (2020) Palarivattom Flyover Scam. https://en.wikipedia.org/wiki/Palarivattom_Flyover_scam

Leave a comment